Bond ladders

Discover how bond ladders can help you secure the predictable income of bonds with the flexibility to reinvest if rates go up.

Ready to create your own bond ladder online? Our new CD & Treasury Ladder Builder can make it simple.

What is a bond ladder?

A bond ladder is a portfolio of individual CDs or bonds that mature on different dates. This strategy is designed to provide current income while minimizing exposure to interest rate fluctuations. Instead of buying bonds that are scheduled to mature during the same year, you purchase CDs or bonds that mature at staggered future dates. Spreading out maturity dates can help prevent investors from trying to time the market. Staying disciplined and reinvesting the proceeds from maturing bonds can help investors to ride out interest rate fluctuations.

What are the primary goals of a bond ladder?

There are two primary goals a bond ladder can help investors achieve.

-

Manage interest rate risk

Manage interest rate riskBy staggering maturity dates, investors avoid getting locked into a single interest rate. A ladder helps smooth out the effect of fluctuations in interest rates because there are bonds maturing every year, quarter, or month, depending on the number of rungs in the ladder. When a bond matures, an investor could reinvest that principal in a new longer-term bond at the end of a ladder. If interest rates have risen, they’ll benefit from a new, higher interest rate and keep the ladder going. If interest rates were to fall, unfortunately the maturing bonds would likely be reinvested at lower rates, but the bonds at the end of the ladder will have likely locked in higher yields already.

-

Manage cash flow

Manage cash flowSince many bonds pay interest twice a year on dates that generally coincide with their maturity date, investors can structure predictable monthly bond income based on coupon payments with different maturity months as well as years.

How is a bond ladder created?

The bond ladder itself is fairly straightforward to create. The overall length of time, spacing between maturities, and types of securities are primary considerations when building a bond ladder. Even in a low or rising interest rate environment, bond ladders can help to balance the need for income while managing interest rate risk.

-

Rungs:

Rungs:Take the total amount that you plan to invest, with the goal of extending the ladder as long as possible. For example, $100,000 to buy individual bonds could be invested with 10 rungs of $10,000 each.

An additional benefit to having at least six rungs is that an investor can create a ladder structured to generate income every month of the year.

-

Spacing:

Spacing:The distance between rungs is determined by the span of time between the maturities of the respective bonds, which can range from months to years. Generally, the spacing should be roughly equal.

Bonds with longer maturities tend to offer higher yields, though shortening the bond maturities generally reduces income and interest rate risk.

-

Materials:

Materials:Just like a real ladder, investors can build their ladders with different materials; in other words, different types of bonds or CDs. Moreover, investors can also utilize the potential tax advantages of municipal bonds, the credit guarantee of U.S. Treasuries, or the generally higher yields of investment-grade corporate bonds.

At Schwab, we generally prefer investors to focus on higher-rated bonds when building a bond ladder. Lower-rated bonds, like high-yield bonds, have a greater likelihood of default, and could negatively impact the goal of steady income and predictable value at maturity.

How does a bond ladder work?

With bond laddering, you invest in multiple bonds with different maturities. As each bond or CD matures, you can reinvest the principal in new bonds with the longest term you originally chose for your ladder.

If interest rates move higher, you can reinvest at higher rates. If rates fall, you'll still have some bonds locked in for the longer term at higher yields.

Here's an example of how a ladder works and is for illustrative purposes only.

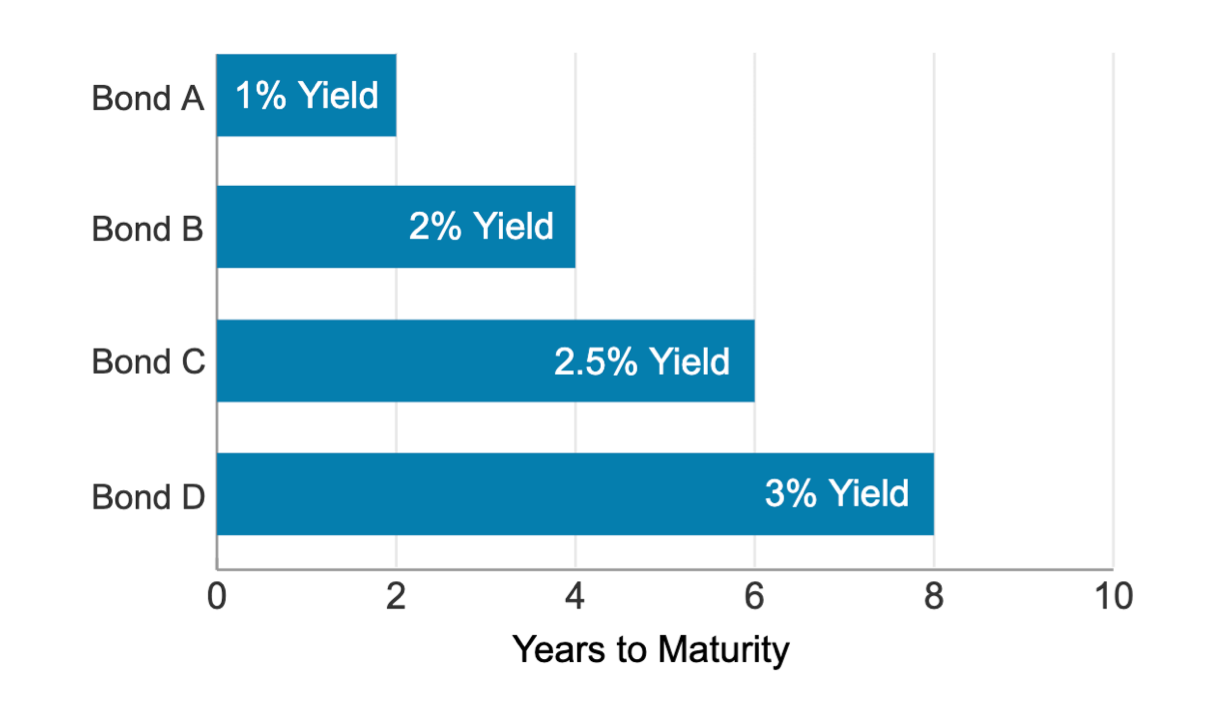

Ladder today

In this example, you buy four bonds with staggered maturities. Your combined average annual yield is 2.125%.

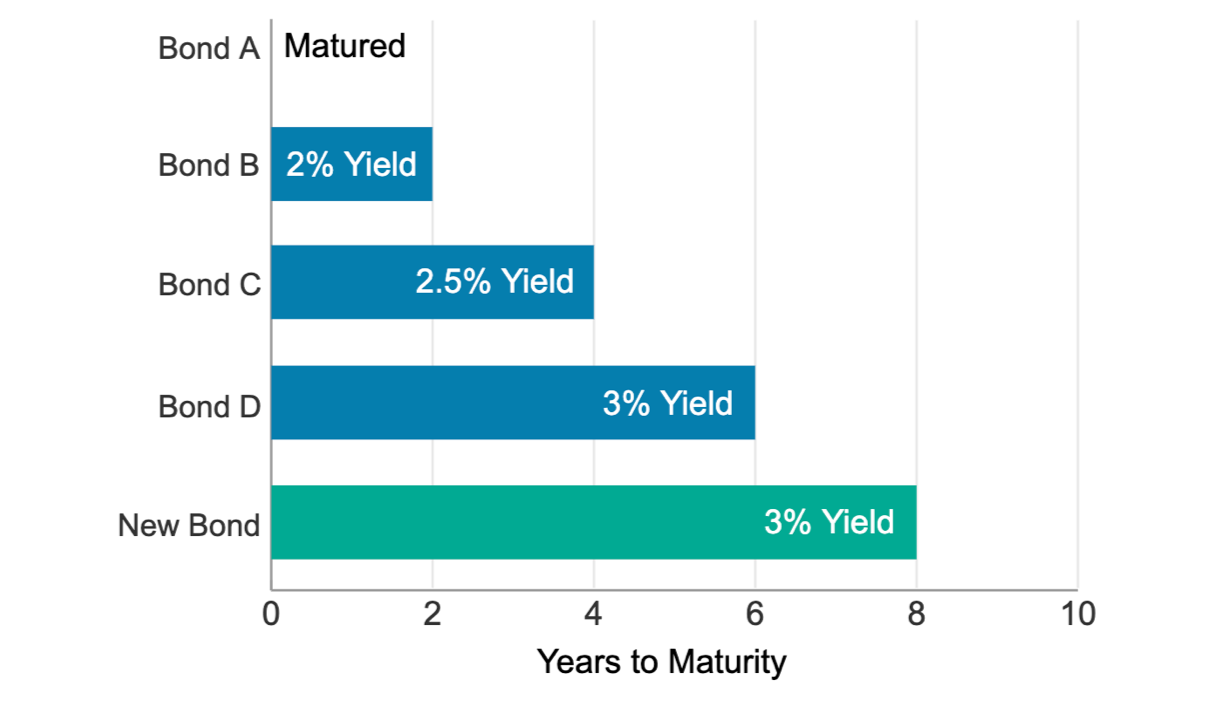

Ladder two years from today

In two years, when Bond A matures, you can reinvest the proceeds in a new bond, extending your ladder. You can continue to do this as bonds mature in the future.

Ready to start investing?

-

Ready to start investing in bonds?

Already a Schwab client? Get started

Have a specialist contact you.

Talk to a Schwab Fixed Income Specialist.

Our specialists offer objective, non-commissioned guidance on a wide range of fixed income products and strategies including ladders, bullets, barbells, and more. You can expect personalized service on topics such as:

- Help with choosing from a wide variety of investment options

- Suggestions for adjusting to changing market conditions

- Assistance with using our online trading features

Call 877-903-8069

Questions? We're ready to help.

-

Call

Call -

Chat

Chat -

Visit

Visit