Welcome USAA members.

Schwab Intelligent Portfolios®

Welcome to automated investing, where our robo-advisor can help build and manage your portfolio.

Our robo-advisor does the work, so you don't have to.

Automated investing with human help when you need it.

- Our robo-advisor builds, monitors, and automatically rebalances a diversified portfolio based on your goals.

- 24/7 live support from U.S.-based service professionals.

- Get started with as little as $5,000.

Backed by our commitment to keeping costs low.

- Pay no advisory fee and no commissions.

- Invest in a portfolio of low-cost

Tooltip

(ETFs).

- Just as if you'd invested on your own, you will pay the operating expenses on the ETFs in your portfolio, which includes Schwab ETFs™.

What else you should know.

We believe cash is a key component of an investment portfolio. Based on your risk profile, a portion of your portfolio is placed in an FDIC-insured deposit at Charles Schwab Bank. Some cash alternatives outside of the program pay a higher yield. Please Note: Charles Schwab & Co., Inc. is not an FDIC-insured bank and deposit insurance covers the failure of an insured bank. Charles Schwab & Co., Inc. is a brokerage firm and a member of SIPC, which provides protection for brokerage account assets. Certain conditions must be satisfied for FDIC insurance coverage to apply. Tooltip

How Schwab Intelligent Portfolios works:

1. Complete a short questionnaire to establish your goals, risk tolerance, and timeline.

2. Get a diversified portfolio of ETFs chosen by experts.

3. Our robo-advisor monitors your portfolio daily and automatically rebalances it as needed.

Compare Schwab Intelligent Portfolios to others

Compare Schwab Intelligent Portfolios to others.

| Schwab Intelligent Portfolios® | Betterment Digital | Wealthfront | Fidelity Go® | E*TRADE Core Portfolios | |

|---|---|---|---|---|---|

| Advisory fees | No advisory fee charged | 0.25% | 0.25% |

No advisory fee <$25,000 0.35% per year $25,000+ |

0.30% |

| Tooltip | |||||

| 24/7 phone and live chat support from U.S.-based service professionals |

Just as if you'd invested on your own, you will pay the operating expenses on the ETFs in your portfolio, which includes Schwab ETFs™.

Competitors' information obtained from their respective websites as of 12/1/25. Pricing and offers are subject to change without notice.

Set your goals and start reaching for them.

Our robo-advisor can help you invest for retirement, college, vacations, building long-term wealth, or creating a sustainable income stream. Here's what you get with Schwab Intelligent Portfolios.

A diversified portfolio, tailored to your needs.

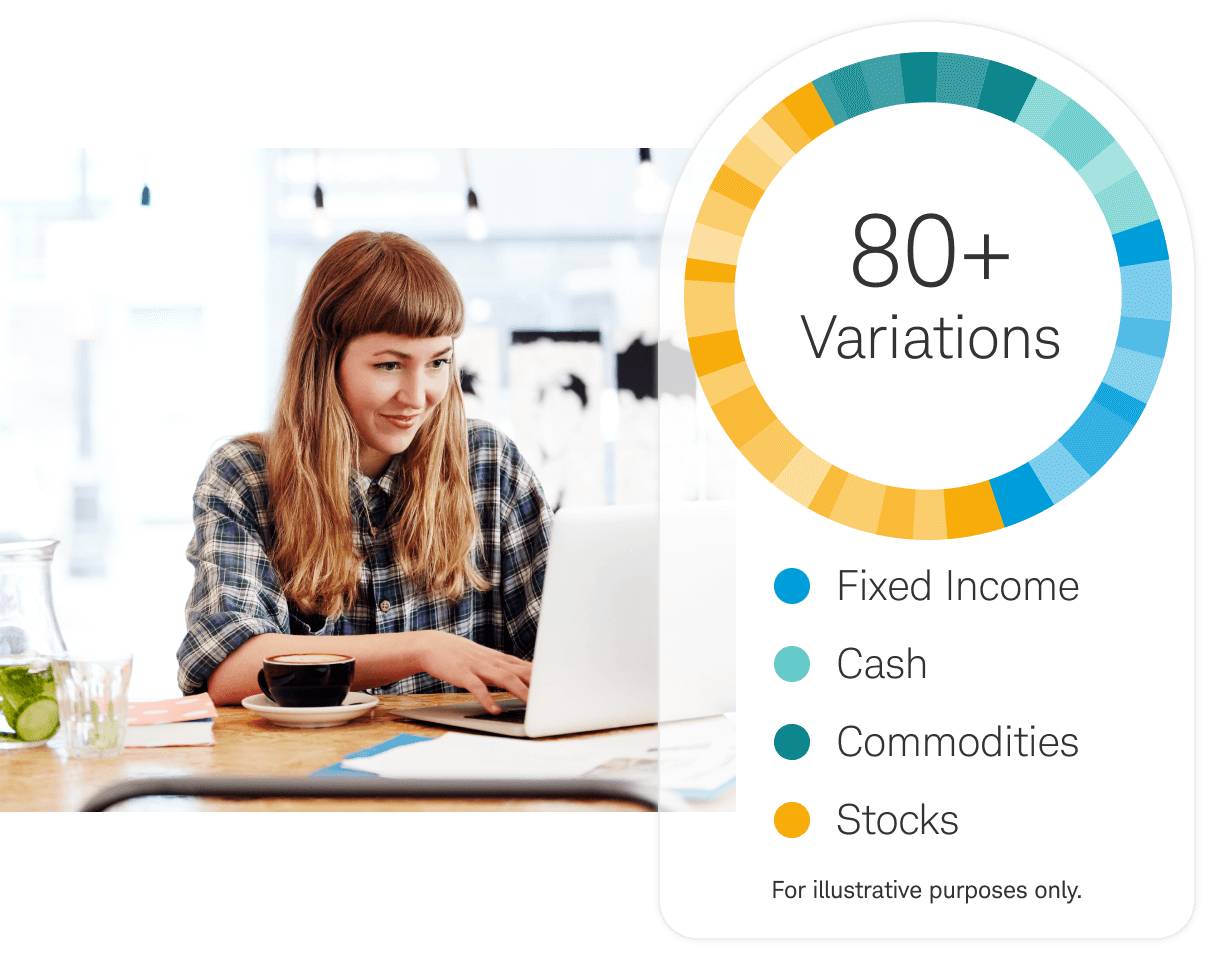

Based on your answers about your goals, risk tolerance, and timeline, Schwab Intelligent Portfolios will provide you a tailored portfolio from more than 80 variations:

- About 50 ETFs Selected and monitored by Schwab experts that span about 20 Tooltip

- Tooltip Global, U.S. Focused, Income Focused

- Tooltip Ranging from Conservative to Aggressive Growth

Want to see the historical average returns and asset allocations of our portfolios?

Tax efficiency.

If an investment declines in value, our automatic tax-loss harvesting can help you offset the taxes on investment gains.

Ready to get started?

Compare us with other firms.

Common questions.

Getting started

You can open a Schwab Intelligent Portfolios account with a minimum of $5,000.

You can have the following account types:

- Taxable: Individual, Joint Tenant, Tenants in Common, Community Property, Custodial, Revocable Living Trust

- Tax-Advantaged: Traditional IRA, Roth IRA, Rollover IRA, Inherited IRA, SEP-IRA, SIMPLE IRA

Of course! After considering your options you can choose a Rollover or Roth IRA account. These rollovers are as simple as contacting your former employer plan administrator or custodian and telling them you want a direct rollover of your plan assets.

Next Steps

- Complete any forms required by your plan administrator or custodian.

- Decide how you want your retirement assets distributed.

- Your Schwab rollover specialist can assist you with questions depositing funds into your Schwab Intelligent Portfolios IRA.

Tips:

- To prevent funds from being taxed, the check should be made payable to "Charles Schwab & Co., Inc., FBO (Your Name)."

- For an easy deposit, give your employer your Schwab Intelligent Portfolios IRA account number and ask them to include it on the check.

- Instruct your plan administrator or custodian to mail the check to: Charles Schwab & Co., Inc., PO Box 2339, Omaha, NE 68103.

If you need help, give us a call at 866-855-9102 to talk to a Rollover Consultant. If you are currently a Schwab Plan participant, please call 800-724-7526.

First, you should identify if you want to enroll a taxable or tax-advantaged account into Schwab Intelligent Portfolios. You can see the types of accounts commonly used below. You will need to have this information when you are completing the online questionnaire to receive a portfolio recommendation.

- Taxable: Individual, Joint Tenant, Tenants in Common, Community Property, Custodial, Revocable Living Trust

- Tax-Advantaged: Traditional IRA, Roth IRA, Rollover IRA, Inherited IRA, SEP-IRA, SIMPLE IRA

To start the process, log in to Schwab.com and navigate to Accounts > Open An Account > Schwab Intelligent Portfolios®. You will enter the online questionnaire to build your portfolio. After you answer all the questions, you will receive a portfolio recommendation. On the next page, select Schwab Intelligent Portfolios, and you will begin the account enrollment process. You will be presented with two options—"Open a new account" or "Enroll an existing Schwab account." Select the latter. On the next page, you will have the ability to select the Schwab account you would like to enroll. Once you follow the prompts to review the appropriate disclosures, your account will be enrolled into Schwab Intelligent Portfolios, and your funds will likely be liquidated from your existing Schwab account and invested into your Schwab Intelligent Portfolios account within 3-5 days.

You can withdraw cash at any time by logging in to your account and requesting a transfer to another Schwab brokerage or Schwab bank account, or to another financial institution. Funds will be available immediately unless the amount that you request to withdraw exceeds the cash allocation in your portfolio. If the withdrawal requires the sale of ETFs to provide the requested cash, the availability of the funds will be delayed until the sale transactions have settled. The processing and settlement takes between 4-6 business days.

After your withdrawal, your portfolio will rebalance as needed to reach its target asset allocation. Your withdrawal may also cause your account to be ineligible for tax-loss harvesting if you have enrolled in the service and your account falls below the minimum.

No, beneficiaries are unique to each account number. You will need to establish new beneficiary instructions for any account you open.

Log in to Schwab.com and navigate to Service > My Profile > Beneficiaries. On this page you can manage your beneficiaries for your eligible accounts.

Costs & fees

You pay no advisory fee and no commissions. Just as if you'd invested on your own, you will pay the operating expenses on the ETFs in your portfolio, which includes Schwab ETFs™. We believe cash is a key component of an investment portfolio. Based on your risk profile, a portion of your portfolio is placed in FDIC-insured Deposit Accounts at Charles Schwab Bank, SSB. Certain conditions must be satisfied for FDIC insurance coverage to apply. Charles Schwab & Co., Inc. is not an FDIC-insured bank and deposit insurance covers the failure of an insured bank. Some cash alternatives outside of the program pay a higher yield.

We are committed to keeping fees low to help you achieve your goals. It starts with not charging an advisory fee or commissions. We can do that because we earn revenue from other sources as detailed below.

- ETFs: Schwab Intelligent Portfolios invests in Schwab ETFs. This creates revenue for Charles Schwab Investment Management, Inc., a Schwab affiliate that receives management fees on those ETFs. Schwab Intelligent Portfolios® also invests in third-party ETFs, and Schwab also receives compensation for providing shareholder services to those third-party ETFs.

- Cash: We believe cash is a key component of an investment portfolio. Based on your risk profile, a portion of your portfolio is placed in FDIC-insured Deposit Accounts at Charles Schwab Bank, SSB. Certain conditions must be satisfied for FDIC insurance coverage to apply. Charles Schwab & Co., Inc. is not an FDIC-insured bank and deposit insurance covers the failure of an insured bank. Some cash alternatives outside of the program pay a higher yield.

- Order Flow: Schwab receives revenue from the market centers where ETF trade orders are routed for execution.

Yes, the interest rate on cash balances in the Sweep Program is set on the first business day of each month equal to the seven-day yield (with waivers) for the Schwab Government Money Fund – Sweep Shares (symbol: SWGXX) as determined at the end of the prior month. See Current Interest Rates for more details. Some cash alternatives outside of the program pay a higher yield.

No, Schwab Intelligent Portfolios has leveraged the power of technology to automate these complex tasks.

Tax-loss harvesting is available for taxable portfolios with $50,000 or more, and there are no additional fees for activating this feature in your account. You must be enrolled for tax-loss harvesting to occur.

Portfolio construction & ETFs

An ETF, or exchange-traded fund, is a basket of securities that gives you exposure to a particular asset class, industry, commodity, or region. We like them because they offer similar diversification as an index mutual fund but unlike index mutual funds, ETFs can be traded at any time during the day. ETFs also offer exposure to a greater breadth of markets, are more transparent in terms of their underlying holdings, and tend to be more tax efficient and low cost.

Both Schwab ETFs™ and third-party ETFs are filtered through a carefully selected set of stringent criteria. This ensures that all ETFs chosen for Schwab Intelligent Portfolios deliver both diversity and cost efficiency.

These selection criteria help pare down the universe of ETFs to about 50 that could potentially be part of your Schwab Intelligent Portfolios account. So, let's examine those criteria and see how that works.

Eschewing risk. Any nonstandard ETFs are eliminated—that is, ETFs that are inverse and leveraged, actively managed, that invest only in one country, or those that have less than three months of history, among other factors.

Size matters. Next, all ETFs without sufficient assets under management are stripped out, because ETFs without sufficient assets are at greater risk of closing.

Monitoring consistency. Schwab Intelligent Portfolios ETFs must closely track the indexes our asset allocation models are based on. This measure is not whether the fund outperforms the benchmark, but rather the degree to which it approximates the index and is a good representation of the asset class.

Low OERs are key. Finally, the selection process focuses on ETFs with low operating expense ratios (OERs) while also meeting the size, tracking, and bid-ask spread criteria. (Source: "How to Choose an Exchange-Traded Fund (ETF)," The Wall Street Journal How-To Guide.)

After the ETFs are chosen, Charles Schwab Investment Management, Inc. ("CSIM") monitors their performance quarterly. CSIM also reviews the ETF selection annually to make sure the ETFs available for Schwab Intelligent Portfolios continue to meet the criteria described above, and can provide consistency and diversity.

Please visit the Schwab Intelligent Portfolios Selection Process page for more information and a representative list of ETFs used in Schwab Intelligent Portfolios.

Asset allocation is the foundation of every well-constructed investment portfolio and is at the heart of the advice we at Schwab give when advising clients on their total portfolio. Because it is so important, we have dedicated an entire team of Charles Schwab Investment Management, Inc. ("CSIM"), experienced analysts to continually use state-of-the-art research and evolve our approach to creating asset allocations designed to improve outcomes for individual investors.

The appropriate asset allocation differs from person to person depending on their situation, risk tolerance, and time frame for their investing goals. The table below shows a sample asset allocation for three individual investors ranging from aggressive to conservative.

- Investor 1: A 30-year old who sees herself as aggressive and is saving for retirement. This investor clearly has a long investment horizon (both for starting to withdraw from this portfolio and the period over which she would need to withdraw). The primary goal is capital appreciation (growth), and her investment strategy is Global Aggressive Growth with Taxable Bonds.

- Investor 2: A 40-year-old father whose tolerance for fluctuations in his portfolio value is above average and is using this account to save for the college expenses of his 3-year-old twins. His goal is a combination of capital appreciation, income and being somewhat defensive. His investment strategy is Global Moderate Growth with Taxable Bonds.

- Investor 3: A tax-sensitive 65-year-old retired investor who is living off her portfolio and wants to reduce portfolio volatility. Her primary goal is to generate adequate income starting now, with some potential for capital appreciation to sustain the portfolio over a long-term. Her investment strategy is Income Focused Moderately Conservative with National Muni Bonds.

| Investor 1 | Investor 2 | Investor 3 | |

|---|---|---|---|

| Stocks | 88.0% | 58.0% | 25.0% |

| US Large Company Stocks | 12.0% | 8.0% | 0.0% |

| US High Dividend Stocks | 0.0% | 0.0% | 11.0% |

| US Large Fundamental | 15.0% | 10.0% | 0.0% |

| US Small Company Stocks | 6.0% | 4.0% | 0.0% |

| US Small Fundamental | 10.0% | 7.0% | 0.0% |

| International Developed Large Company Stocks | 8.0% | 5.0% | 0.0% |

| International Developed Large Fundamental | 9.0% | 5.0% | 0.0% |

| International Developed Small Company Stocks | 4.0% | 3.0% | 0.0% |

| International Developed Small Fundamental | 4.0% | 3.0% | 0.0% |

| International High Dividend Stocks | 0.0% | 0.0% | 11.0% |

| International Emerging Market Stocks | 6.0% | 4.0% | 0.0% |

| International Emerging Market Fundamental | 10.0% | 7.0% | 0.0% |

| US Exchange Traded REITs | 2.0% | 1.0% | 2.0% |

| International Exchange Traded REITs | 2.0% | 1.0% | 1.0% |

| Investor 1 | Investor 2 | Investor 3 | |

|---|---|---|---|

| Fixed Income | 3.1% | 31.5% | 58.0% |

| US Treasuries | 0.0% | 2.0% | 0.0% |

| US Investment Grade Corporate Bonds | 3.1% | 12.0% | 0.0% |

| US Securitized Bonds | 0.0% | 3.0% | 0.0% |

| US Inflation Protected Bonds | 0.0% | 12.5% | 20.0% |

| International Developed Country Bonds | 0.0% | 0.0% | 2.0% |

| US Corporate High Yield Bonds | 0.0% | 1.0% | 1.0% |

| International Emerging Market Bonds | 0.0% | 1.0% | 1.0% |

| Investment Grade Muni Bonds | 0.0% | 0.0% | 31.0% |

| Preferred Stocks | 0.0% | 0.0% | 1.0% |

| Bank Loan and other Floating Rate Notes | 0.0% | 0.0% | 2.0% |

| Investor 1 | Investor 2 | Investor 3 | |

|---|---|---|---|

| Commodities | 2.0% | 1.0% | 0.0% |

| Gold & Other Precious Metals | 2.0% | 1.0% | 0.0% |

| Investor 1 | Investor 2 | Investor 3 | |

|---|---|---|---|

| Cash | 6.9% | 10.5% | 15.0% |

Learn more by visiting this asset allocation white paper.

Cash investments play an important role within a well-diversified portfolio and serve several purposes, including:

- Greater stability

- Liquidity

- Diversification

- Potential inflation protection

A cash allocation provides stability to help mitigate downside risk. Lower portfolio risk can help moderate downturns and keep investors focused on their longer-term goals. Cash allocations are determined according to an investor's risk profile, with the most risk-averse or short-term portfolios holding the highest levels of cash and the least risk-averse or longer-term ones holding the lowest levels of cash.

Cash in Schwab Intelligent Portfolios provides an additional layer of stability in the form of FDIC insurance of up to $250,000 per depositor, as it is "swept" into deposit accounts at Schwab Bank, where it also earns a market rate of interest for highly liquid cash investments. Certain conditions must be satisfied for FDIC insurance coverage to apply.

Portfolio management

An automated system monitors your portfolio closely—this includes:

- Rebalancing as needed: Your portfolio won't trade every day, however we perform daily check-ins. When an asset class exceeds its allocated portion in your portfolio, the excess ETF shares are sold, and the proceeds are used to buy positions that have fallen below their target percentage; this keeps your portfolio consistent with your Investor Profile.

- Professional oversight: Periodic evaluations are performed to ensure that your asset allocation represents the right mix of risk and return. The ETFs included in Schwab Intelligent Portfolios are also evaluated to ensure that they continue to meet the stringent selection criteria.

- Tax-loss harvesting: If you have an account with $50,000 or more in assets, and you've elected to automate tax-loss harvesting, your account will be tracked daily for opportunities to offset capital gains by strategically realizing losses.

Every portfolio has a target asset allocation—a combination of stocks, bonds, and cash determined by the investor's stated goals, risk tolerance and time horizon. Over time, however, contributions/withdrawals, gains, and losses cause your portfolio to stray from the original target and become unbalanced.

The solution is rebalancing—the act of periodically buying or selling assets to restore your portfolio to its original target allocations. Schwab Intelligent Portfolios automatically rebalances accounts thanks to an algorithm that adjusts your account when an asset class shifts above or below its target range.

Learn More:

Rebalancing in Action

The primary purpose of rebalancing is to keep your portfolio's asset allocation consistent with your targeted level of risk as markets fluctuate over time. The recommended allocation for your portfolio is based on your goal, time horizon, and risk profile.

Schwab Intelligent Portfolios are monitored and automatically rebalanced as needed to keep the allocation consistent with the client's risk profile as markets fluctuate over time. Portfolio allocations are not adjusted tactically based on short-term views about the markets. In a normal environment, rebalancing happens a few times per year; during more volatile times, don't be surprised if this number increases.

Tax-loss harvesting can help offset capital gains and lower your taxable income by automatically selling an ETF that has fallen enough below the price you paid for it and replacing it with an alternate ETF in the same asset class to keep your portfolio's allocation consistent.

Periods of elevated market volatility highlight the potential benefit of tax-loss harvesting as the number of these trades have historically surged when markets turn turbulent. The goal of the Schwab Intelligent Portfolios algorithm is to maintain a portfolio that closely tracks the investor's strategic asset allocation and captures tax-deductible losses while generally preventing wash sales in your account. As it’s a complicated and time-consuming process, Schwab Intelligent Portfolios has automated this process.

The Sweep Program is a feature that allows for the cash allocation in your Schwab Intelligent Portfolios account to earn interest by being "swept" to a FDIC-insured deposit account at Schwab Bank. The interest rate on cash balances in the Sweep Program is set on the first business day of each month equal to the seven-day yield (with waivers) for the Schwab Government Money Fund – Sweep Shares (symbol: SWGXX) as determined at the end of the prior month. See Current Interest Rates for more details. You can view the cash allocation on your portfolio dashboard at Intelligent.Schwab.com. You can withdraw cash from your Schwab Intelligent Portfolios account at any time by logging in to your account and requesting a transfer. Please Note: Charles Schwab & Co., Inc. is not an an FDIC-insured deposit account at Charles Schwab Bank, SSB. Charles Schwab & Co. Inc. is not an FDIC-insured bank and deposit insurance covers the failure of an insured bank. Charles Schwab & Co., Inc. is a brokerage firm and a member of SIPC, which provides protection for brokerage account assets. Certain conditions must be satisfied for FDIC insurance coverage to apply. Non-deposit products are not insured by the FDIC; are not deposits; and may lose value.