Schwab Intelligent Portfolios: Our Approach to Portfolio Construction

Key Points

- A belief that investors should be well diversified within and across asset classes is core to the Schwab Intelligent Portfolios® strategy.

- Our state-of-the-art portfolio construction approach addresses some of the shortcomings of Modern Portfolio Theory (MPT) and Mean-Variance Optimization (MVO)

- We make conservative assumptions about future returns, risk, extreme events, and correlations, and test the performance of our portfolios over a range of hypothetical scenarios.

Introduction

In a previous paper, we explained the theory and benefits of diversification, as well as the broad universe of asset classes that Schwab Intelligent Portfolios invests in. This paper focuses on portfolio construction – how to combine these asset classes in a manner that is mindful of various market conditions and strikes the right balance between investment risk and return.

We will provide a quick overview of the landscape and history of portfolio construction, and will call out some of the limitations and criticisms of Modern Portfolio Theory along the way. This paper will also highlight 21st century challenges and new market realities and explain how Schwab Intelligent Portfolios attempts to address these when building portfolios.

A brief history of modern portfolio theory

In 1952, economist Harry Markowitz first introduced the concept of diversification, "the only free lunch in finance." Markowitz's work, which served as the foundation for Modern Portfolio Theory, concluded that an investor could reduce the overall risk of a portfolio by including investments that have low correlations to one another.1 His work suggested that investors should construct portfolios with an objective to maximize the expected portfolio return while minimizing the expected portfolio risk. This concept paved the way for the ubiquitous portfolio construction technique known as "Mean-Variance Optimization," which uses industrial optimization methods to find the combination of securities that achieve the objective stated above. Risk, in the context of MVO, is measured by the variance of portfolio returns. The square root of this value, or standard deviation, is more commonly referred to in finance as "volatility" (more on this later).

In 1964, Bill Sharpe built upon this concept and introduced what is known as the Capital Asset Pricing Model (CAPM), which describes the relationship between risk and return, and introduced "beta" as a measure of sensitivity to market risk.2 He concluded that an investor can increase expected returns only by taking on greater market risk. Markowitz and Sharpe won the Nobel Prize in Economics in 1990 for their significant contributions to MPT.

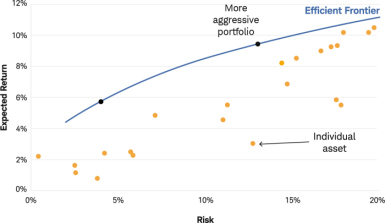

The chart below is known as the "efficient frontier" and plots the "efficient" or optimal combinations of securities which maximize return for a given level of risk.

Exhibit 1: Sample Efficient Frontier

Modern Portfolio Theory in the 21st century: What's wrong with MVO?

While some challenged these findings over the years, it wasn't until after the 2008 financial crisis that the merits of MPT were widely questioned. Critics pointed to the inability of MPT to model such extreme events (so-called "fat tails"), and increased correlations between asset classes during periods of market stress—essentially undermining diversification benefits when investors need them the most.

It's important to note that MPT and the benefits of diversification still hold true to this day. So long as assets don't move in perfect lockstep, it's better not to put all of your eggs in one basket. But what we have learned from more recent financial market dislocations such as the 2008 financial crisis and the 2020 novel coronavirus pandemic is that how we model and measure financial returns and risks (and any benefits from diversification) is increasingly important.

Financial markets have changed a great deal since the 1950s, which has created new challenges and brought to the forefront some of the limitations and simplifying assumptions of MPT. We address these in turn below and highlight how our approach to portfolio construction attempts to address some of these new world challenges and market realities.

Equity and bond returns are expected to be lower than historical averages

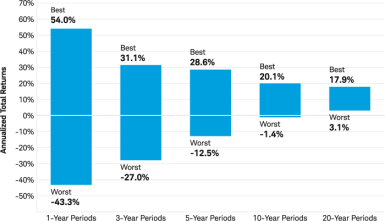

The starting point of most portfolio construction processes is some forecast or estimate of future returns. Large emphasis should be put on the word estimate, as nobody knows exactly how the S&P 500 is going to perform next year (and you should be skeptical of anyone who tells you otherwise). Financial markets are complex and intertwined, driven by human behavior, and are constantly evolving – making them inherently impossible to predict, especially over short horizons. What we do know, however, is that predicting long-term averages is easier than predicting short-term performance. With advances in technology and productivity leading to economic growth, theory tells us that, over long periods, markets should go up more than they go down. It's why Charles Schwab & Co., Inc. ("Schwab") and Schwab Intelligent Portfolios take a long-term view on the markets and advocate for goals-based financial planning and investing, and avoiding a focus on short-term performance. The chart below illustrates this point by showing the range (best and worst) of average annual returns of the S&P 500 Index from 1926 – 2019. The best annual return over this period was 54% and the worst was -43.3%.3 It's not hard to see how predicting 1-year returns could be difficult given the disparity! If instead we look at, say, 10-year periods: the best average annual return is 20.1% and the worst is -1.4%, a much smaller range and therefore much easier to forecast.

Exhibit 2: Lengthening holding period may reduce downside risk

Diversified equity portfolio as represented by the S&P 500® Index (1926–2019)

Source: Schwab Center for Financial Research with data provided by Standard and Poor's. Every 1-, 3-, 5-, 10-, and 20-year rolling calendar period for the S&P 500 Index was analyzed from 1926 through 2019. The highest and lowest annual total returns for the specified rolling time periods were chosen to depict the volatility of the market. Returns include reinvestment of dividends. Indices are unmanaged, do not incur fees or expenses, and cannot be invested in directly. For additional information, please see Schwab.com/IndexDefinitions. Past performance is no guarantee of future results. Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

As highlighted in this article, we also have strong economic reasons to believe that, going forward, average equity and bond returns will be lower than their historical averages. As the mantra goes, "past performance is no guarantee of future results." Merely extrapolating from stocks and bonds' long-term historical performance will not be sufficient for asset allocation and portfolio construction going forward. As such, Schwab Intelligent Portfolios makes use of the large body of work that goes into Schwab's capital market return estimates and relies on these forward looking, long-term, estimates to inform our portfolio construction process.

Market returns are not normally distributed

Global interconnectivity and the speed of information are making markets increasingly more volatile as major market-moving shocks have increased in number and intensity in recent years. Financial, fiscal, political and pandemic events such as the 2010 European debt crisis, the 2016 referendum on Brexit and related wave of global populism, the COVID-19 global pandemic and the disruptions in supply chains that began in 2020, and more recently, the 2022 Russia-Ukraine conflict have unnerved investors and roiled financial markets.

Nassim Taleb used the term "black swan" in his New York Times best-selling book to describe the extreme impact of rare and unpredictable events. Due the outsized impact extreme events can have on financial goals, it is critically important for portfolio construction methods to be mindful of (and, to the extent possible, model) these extreme "tail," or rare events.

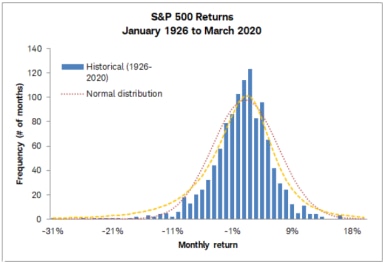

Unfortunately, a simplifying assumption made by MVO (and, more generally throughout finance) is that financial returns can be well approximated by a bell-shaped "normal" distribution. This assumption has come under heavy criticism since the 2008 financial crisis as it has been empirically demonstrated that returns exhibit "fat tails" and negative "skew,"4 portfolios constructed based on a normal distribution can underestimate both the incidence and magnitude of such rare tail events.

In order to address this, Schwab Intelligent Portfolios utilizes statistical methods and assumptions that can adequately represent the empirically observed skewed and fat-tailed nature of financial returns. The result is a portfolio that is constructed based on more realistic assumptions about extreme values and financial market dislocations (that should now be expected to be the norm). To illustrate this, the chart below shows the frequency of monthly returns of the S&P 500 from January 1926 to March 2020. The dotted red line is how a "normal" distribution would approximate the S&P 500. If you look closely, you may notice that this line underestimates the frequency of large negative returns (those that have actually occurred). The yellow line is the "fat-tailed" approximation that we use to construct your portfolio – a meaningfully more conservative assumption about the frequency of "outliers" or extreme events.

Exhibit 3: S&P 500 returns: January 1926-March 2020

Source: Charles Schwab Investment Management, Inc. and Morningstar Direct

Volatility is an incomplete measure of risk

In a related fashion, the conventional way "risk" is measured in MPT and throughout finance is based on the statistical concept of variance or standard deviation. You may recall from a math class you took in high school that standard deviation is a measurement of the average absolute deviation from the mean.5 Volatility (standard deviation of returns) is an incomplete measure of risk in a couple regards. For one, as introduced previously, volatility focuses on the "middle" of the distribution and ignores the "tails." We have already talked about the outsized impact extreme events can have on wealth and financial goals. Second, volatility penalizes above average returns equally as below average returns. Said differently, it is symmetric. It might be OK to ignore these two shortcomings when returns are assumed to follow a (symmetric) normal distribution but, in the presence of skewed and fat-tailed returns, it's easy to understand how focusing solely on volatility may not tell the whole story.

We advocate for using a more comprehensive, downside risk metric known as "expected shortfall" or "Conditional Value at Risk" (CVaR) as part of portfolio construction. CVaR is a measurement of the size of extreme losses, the ones you should care about. Whereas standard deviation is a measurement of the typical variation around the average – the "noise" you should expect.6

Correlations are higher and tend to rise during crises

As highlighted in this paper, diversification offers substantial benefits. The diversification benefits associated with combining assets into a portfolio are driven primarily by how closely the returns on those assets move together. When two assets move perfectly positively correlated (correlation of +1), there are no benefits from combining them in a portfolio. When two equally risky assets are perfectly negatively correlated (correlation of -1), combining the two assets into a portfolio can help eliminate volatility. A correlation of zero means that the two assets are uncorrelated and don't move together at all. In reality, no two assets are perfectly correlated—either positively or negatively— and most correlations are positive. Investors should, ideally, seek investments with lower correlation to one another.

Assets have become more highly correlated in recent years. This could be attributable to a number of factors, but most certainly it is due to greater inter-connectivity between global markets. Multinational corporations have proliferated to such an extent that what happens in Europe and Asia impacts the U.S. markets and vice versa. Many Fortune 100 companies in the United States depend on emerging markets for growth and supply chains, and many overseas corporations depend on demand from American consumers. In addition, trade, e-commerce, and the internet are fueling further inter-connectivity.

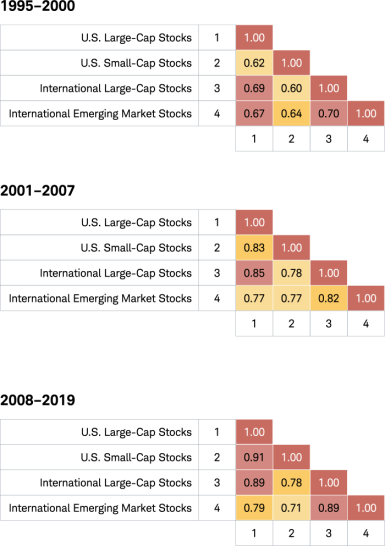

The correlations for four equity asset classes over three different time periods are shown below. As you can see, correlations have generally been rising since 1995-2000 (as seen below by the increasing amount of red and orange squares). This means diversification benefits have been decreasing over time.

Exhibit 4: Asset class correlations: 1995-2019

Source: Charles Schwab Investment Management, Inc. and Morningstar Direct. See disclosures for proxy indices.

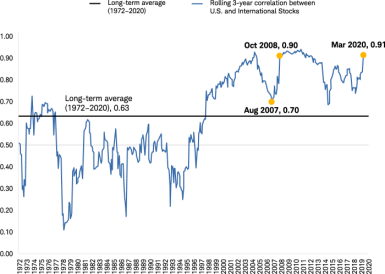

Not only are correlations higher, but they can vary over time and, most importantly, tend to rise in times of crisis. The chart below shows the estimated correlation between U.S. and international stocks from 1972 to 2020. You can see that the long-term average correlation between these two similar asset classes is 0.63, but this has been steadily rising since the turn of the millennium and spiked to as high as 0.90 in the wake of the 2008 financial crisis (and subsequently fell and spiked again during the COVID-19 pandemic in 2020).

Exhibit 5: Estimated correlation between U.S. and international stocks: 1972-2020

Source: Charles Schwab Investment Management, Inc. and Morningstar Direct

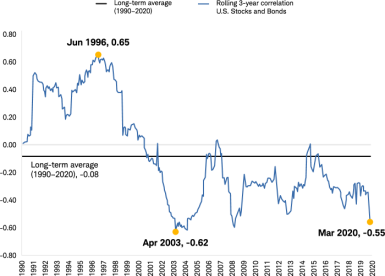

Similarly, the chart below shows the same for U.S. stocks versus U.S. bonds. The common assumption in finance and portfolio construction is that stocks and bonds are negatively correlated (remember: negative correlations are a good thing for diversification). However, it's important to point out that depending on the time period which correlations are measured, the stock/bond correlation could be positive or negative.

Exhibit 6: Estimated correlation between U.S. stocks and bonds: 1972-2020

Source: Charles Schwab Investment Management, Inc. and Morningstar Direct

How does all of this relate to MPT and why should you care? Again, MVO is limited in that it assumes that correlations are fixed (and are typically estimated based on a long-term average, e.g., something like the black line in the charts above). For portfolio construction, it is critical to incorporate dynamically changing correlations, especially during extreme market conditions. Failing to do so can materially underestimate risk and any perceived benefits from diversification when they are needed the most. Schwab Intelligent Portfolios uses an increasingly popular and more comprehensive statistical technique known as a "copula" to model variations in correlations, especially during extreme events, resulting in a portfolio that is constructed based on more realistic and dynamic assumptions about correlations and diversification.

Putting all the pieces together

Schwab Intelligent Portfolios recognizes the constantly evolving nature of financial markets and the difficulty and futility in trying to predict short-term performance. Rather than relying solely on historical data or static inputs, we take a probabilistic or scenario-based approach to portfolio construction. We use fat-tailed distributional assumptions to simulate 10,000 hypothetical future realizations of returns, allowing for changing correlations along the way. We use our forward-looking capital market estimates to inform the general direction of these hypothetical returns, but the probabilistic approach allows for a lot of variation (both good and bad scenarios).

Then, using mathematical optimization, we find portfolios that perform relatively well across all of the simulated histories, finding the right mix between return and downside risk (CVaR). The benefit of such an approach is that our portfolios are constructed using conservative assumptions about future returns, risk, extreme events, and correlations. And their performance is tested over a large range of hypothetical scenarios and outcomes.

Expert judgment

Our stress-tested models are overseen by experts within Charles Schwab Investment Management, Inc. who are constantly reviewing assumptions, inputs and, most importantly, the composition of your portfolio.

Conclusion

Forecasting financial markets is tough, perhaps impossible. Over the long-term, however, economic theory tells us that markets should go up more than they go down. Modern Portfolio Theory and Mean-Variance Optimization were ground-breaking innovations in the realm of portfolio construction. But the foundation set forth by MPT is not without cracks. Schwab Intelligent Portfolios attempts to address some of these limitations and takes a humble approach to portfolio construction by making conservative assumptions about returns, correlations, and measurements of risk.